Five year, geared, buy-to-let investments have continued to provide excellent profits with an annual rate of return of 11.28% last quarter. This is the fifth quarter where returns have exceeded 11%. Once again, these returns are principally a result of continuing property price inflation.

Compared with recent history, when returns fluctuated wildly following the credit crunch, returns have now stabilised at a relatively high level, compared to other forms of investment. Even without the effects of gearing, cash buyer landlords saw returns of 5.93% over the same quarter.

Pundits in the buy-to-let sector see further growth in 2015. Our figures suggest the market is continuing to offer consistent returns. However various factors could cause this to change.

Amendments to the pensions system from April may cause an inflow of cash buyers, triggering an asset price bubble in an already overvalued market. This would result in further capital gains for established landlords in the short term with other, perhaps unforeseen, effects subsequently.

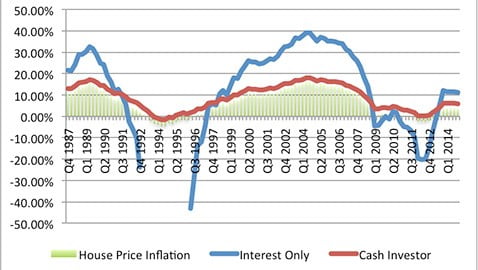

The graph below expresses quarterly five year, geared and cash investor buy-to-let profitability levels since Q4 1987, and five year property price inflation levels expressed as a compound annual rate.

This graph highlights the volatility of the market, particularly for geared investors. Between Q1 1992 and Q1 1996 an average five year, geared investor would have found themselves in negative equity.

The reason for these losses was a boom and bust in the market caused by mass buying following the telegraphing of the end of joint MIRAS in August 1988. Buy-to-let investors buying at the peak suffered the consequences selling five years later. There are parallels between this influx of new buyers and the possible influx of new buy-to-let investors following changes to the pension system.

The boom and bust of 1988 was followed by interest rate spikes as a result of Black Wednesday in September 1992. It took the market 10 years to recover. Such huge fluctuations seem unlikely today but rising rates are definitely a factor to be considered when making investment decisions.

Prospective new entrants to buy-to-let must consider all the issues. Most would benefit significantly from professional guidance from experts including mortgage brokers. History tells us that periods of stability, like the one we are currently experiencing, are the exception rather than the rule.

Our index uses Bank of England, Nationwide and Association of Residential Letting Agents data to calculate the historic returns over 25, 20, 15, 10, and 5 year periods, for a cash buyer or a geared investor, with a repayment or an interest only mortgage, selling today.

Brian Hall is founder of The Model Works